English

English

Ivonescimab in NSCLC: Clinical Validation, Market Scenarios & Commercial Strategy

Price range: $1,500.00 through $3,500.00

A strategic market intelligence report on Ivonescimab/AK112 in NSCLC, covering clinical validation, competitive positioning, regulatory catalysts, KOL sentiment, payer access, revenue scenarios, and commercial strategy after ASCO 2026.

Description

The Drug That Beat Keytruda. The Trial That Determines Everything. The Window That Closes in Months.

On May 31, 2026, a China-originated cancer therapy headlined an ASCO Plenary for the first time in 61 years. The drug: ivonescimab, a tetravalent PD-1/VEGF bispecific. The result: a statistically significant overall survival victory over PD-1 plus chemotherapy in first-line squamous NSCLC—something no drug had ever achieved.

Four weeks later, the stock of its Western partner, Summit Therapeutics, had dropped 23% on an interim analysis miss in the global HARMONi-3 trial. The market confused statistical methodology with biological failure. Sophisticated investors recognized the opposite: a buying opportunity in a drug whose mechanism was validated, whose Western data remained pending, and whose probability-weighted expected value suggested 50%+ upside at prevailing prices.

This is the central tension of the ivonescimab story—and the reason this report exists.

Ivonescimab, also known as AK112/SMT112, has become one of the most closely followed immuno-oncology assets in non-small cell lung cancer. With pivotal clinical readouts, global regulatory catalysts, China commercial experience, competitive pressure from emerging PD-1/VEGF bispecifics, and major implications for the Keytruda-era treatment paradigm, the asset now sits at a critical strategic inflection point.

This Mellalta Market Intelligence report provides a structured, commercially focused assessment of Ivonescimab’s opportunity in NSCLC. It examines the clinical evidence, upcoming catalysts, treatment algorithm implications, payer and HTA outlook, competitive threats, business development relevance, and revenue scenarios — without relying on surface-level data summaries.

Designed for decision-makers, the report translates complex oncology data into practical strategic intelligence for commercial planning, licensing decisions, portfolio strategy, investment evaluation, and competitive intelligence.

What This Report Helps You Understand

- Why Ivonescimab has become a major strategic topic after ASCO 2026

- How the HARMONi clinical programme could reshape NSCLC treatment positioning

- Where the opportunity may sit across EGFR post-TKI, squamous, non-squamous, and PD-L1-defined populations

- What key opinion leaders and analysts are watching closely

- How regulatory, payer, HTA, and access dynamics may influence commercial uptake

- Which competitive assets could challenge the PD-1/VEGF bispecific space

- What scenarios could determine whether Ivonescimab remains a niche asset, segment leader, or broader oncology franchise

Key Report Modules

- Clinical Intelligence

Assessment of Ivonescimab’s NSCLC evidence base, mechanism of action, pivotal trial programme, and clinical differentiation. - Market & Revenue Strategy

Scenario-led commercial outlook, patient funnel logic, peak revenue considerations, and adoption pathway analysis. - Competitive Landscape

Evaluation of current standards of care, Keytruda exposure, emerging PD-1/VEGF bispecific competitors, ADC threats, and future treatment algorithm shifts. - Regulatory & Access Outlook

US FDA review considerations, global regulatory pathways, payer access dynamics, HTA implications, and launch readiness factors. - KOL & Analyst Sentiment

Balanced review of bullish and sceptical viewpoints shaping prescriber confidence, investor expectations, and market adoption. - Business Development Intelligence

Strategic implications for licensing, acquisition interest, partnership timing, and large pharma positioning.

Chapter in Details

- Clinical Foundation (Chapters 1–4)

HARMONi-6’s OS HR 0.66. HARMONi-2’s 49% PFS reduction versus Keytruda. HARMONi’s North American subgroup OS HR 0.70—the data point that directly counters the “China-only” bear case. The 70,000-patient real-world safety database. Each trial is deconstructed with the “Why the Reader Should Care” standard: every hazard ratio mapped to revenue, every subgroup to addressable market, every safety signal to formulary risk. - The HARMONi-3 Prediction Engine (Chapters 5–6)

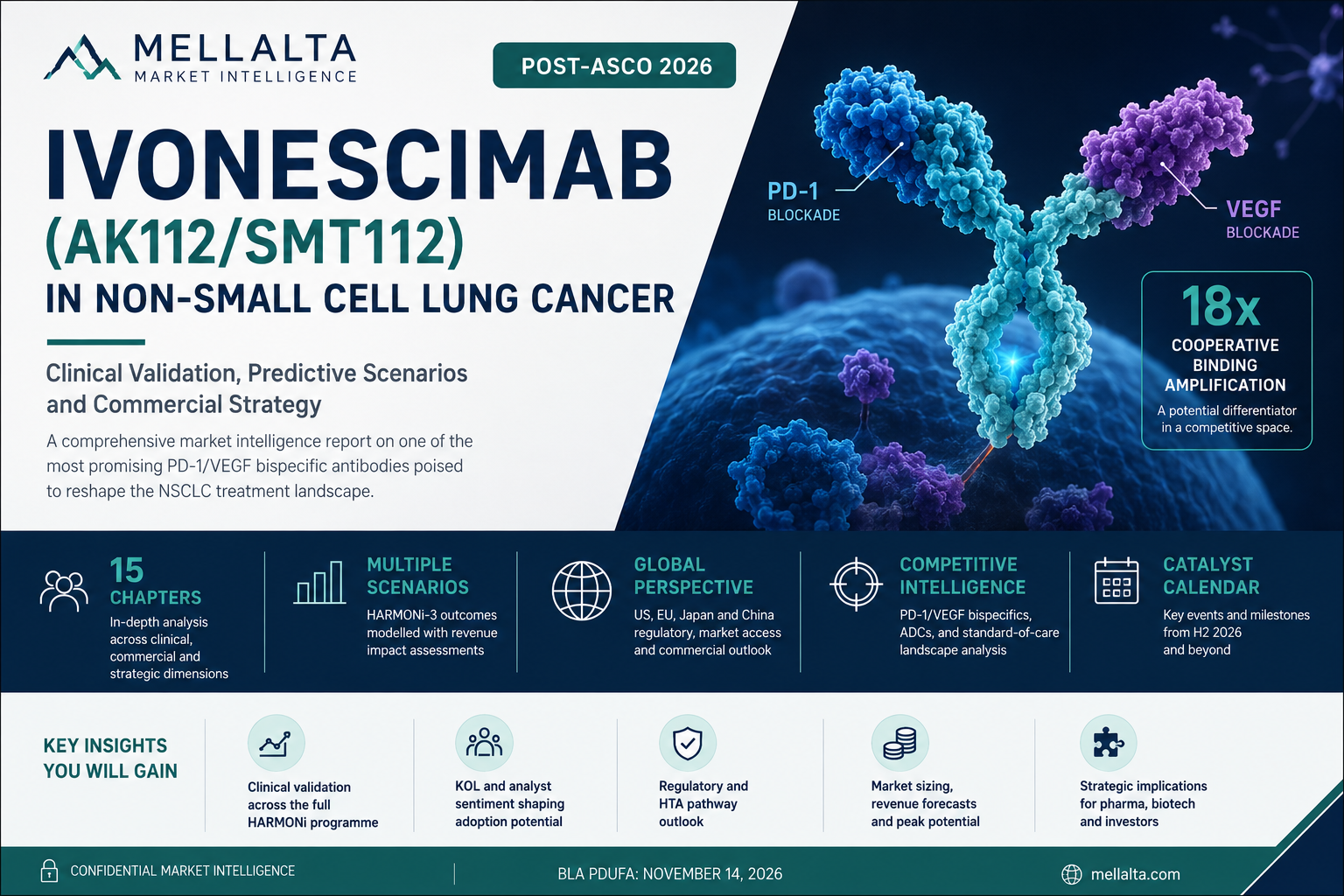

Five scenarios with assigned probabilities, updated post-ASCO 2026. Scenario A (35%): PFS HR 0.70–0.76, Western attenuation but approval. Scenario B (28%): HR 0.62–0.68, mechanism fully translates. Scenario D (10%): the Brahmer hypothesis confirmed, franchise collapses to EGFR niche. The probability-weighted expected peak U.S. revenue: $978 million—but with scenario-dependent ranges from $197M to $1.4B. This is not speculation. It is a decision tool for position sizing, partnership timing, and commercial contingency planning. - Mechanism as Moat (Chapter 3)

The 18x cooperative binding amplification—confirmed by mass photometry, protected by composition-of-matter patents, physically impossible to replicate with separate antibodies. The Pennell-Bteich critique addressed directly: if this were “just bevacizumab,” squamous patients would be bleeding at 31% rates. They are bleeding at 2.6%. The safety-efficacy paradox is the smoking gun. - KOL Sentiment as Leading Indicator (Chapter 7)

41 named oncologists across four prescribing camps. Julie Brahmer’s podium statement—”only effective for Chinese patients”—that appeared in zero press releases. Eric Singhi’s sequencing question: “Where will this drug fit in our evolving 2L+ landscape?” The conversion value of shifting 35% wait-and-see neutrals to believers: $1.2–1.9 billion in NPV acceleration. - Regulatory Architecture (Chapter 8)

The 13-year IRA biologic negotiation shield. The 48-hour NCCN submission window post-PDUFA. The Germany AMNOG gauntlet that determines European and Japanese pricing through foreign reference adjustment. The mid-cycle communication in August 2026 that will move the stock 10–15% on management tone alone. - Revenue Model with Teeth (Chapter 9)

Seven-layer patient funnel from 236,000 annual U.S. NSCLC incidence down to 9,600 addressable EGFR post-TKI patients. Net price assumptions benchmarked to CMS ASP data. Gross-to-net leakage analysis: how 25% rebate erosion silently destroys $132M annually at 10,000 patients. The $978M central estimate—and the sensitivity matrix showing how each assumption shifts it. - The Sacituzumab Tirumotecan Earthquake (Chapter 11)

The ASCO result most commercial teams missed: sac-TMT plus Keytruda achieving PFS HR 0.35 in first-line PD-L1-positive non-squamous NSCLC—published in The Lancet two days before the HARMONi-6 plenary. The three-way 2028 market partition: sac-TMT owns PD-L1-positive non-squamous, ivonescimab owns PD-L1-negative and squamous, biosimilars capture the residual. Any model that does not incorporate this competitive variable is modelling the wrong landscape. - Deal Intelligence (Chapter 13)

The $5B Akeso-Summit benchmark. The $310M of Bob Duggan’s personal open-market purchases—insider buying as signal, not noise. The optimal acquisition window: November 2026 PDUFA to HARMONi-3 readout, when uncertainty is partially resolved but not fully priced. The five ranked strategic acquirers and their fit rationale. - Strategic Implications (Chapter 15)

Tailored recommendations for commercial teams, BD professionals, equity research, market access, R&D pipeline strategists, competitive intelligence, and biotech ecosystem investors. Each audience receives specific, actionable guidance—not generic observations.

The Asymmetric Opportunity

Ivonescimab is not a coin flip. It is a probability distribution with defined boundaries—and the market, as of June 2026, is pricing it closer to the bear case than the weighted expected value justifies.

The mechanism is validated. The cooperative binding is quantified. The 70,000-patient safety database is unprecedented for a pre-Western-approval drug. The PDUFA date is legally binding. The HARMONi-3 trial continues per iDMC recommendation. The North American subgroup already showed OS HR 0.70.

What remains uncertain is magnitude, not existence. The difference between HR 0.70 and HR 0.85 is the difference between a $1.1B franchise and a $675M niche. Both outcomes are investable. Neither is a zero. The only losing strategy is analytical paralysis until the data resolves—at which point the opportunity is arbitraged away.

What You Receive

- 150+ pages across 15 chapters with integrated cross-referencing

- Probability-weighted scenario framework with updated post-ASCO 2026 probabilities

- Named KOL registry with camp assignments and conversion triggers

- Eight-market payer access roadmap (US, UK, Germany, France, Italy, Spain, Japan, China)

- Competitive landscape across four time horizons (2026–2030)

- Sensitivity matrices for revenue, royalty, and valuation assumptions

- Decision dashboard: what to watch, when, and what it means

The Window Closes December 2026

After PDUFA and HARMONi-3 resolution, the information asymmetry that generates alpha disappears. The acquisition premium compresses. The partnership terms harden. The commercial positioning becomes reactive rather than proactive. Can Ivonescimab translate clinical promise into global commercial impact? Can it challenge established PD-1 standards? And what must stakeholders watch before the next major value inflection?

For BD teams: The pre-data window is when valuation gaps are widest and negotiation leverage is highest.

For investors: The probability-weighted expected value exceeds the current market price under reasonable assumptions—but only until the distribution collapses to a single outcome.

For commercial teams: The first 90 days post-approval determine long-term market share. Preparation must begin before the data, not after.

Ideal Buyers

- Pharma strategy teams

- Oncology commercial planning teams

- Business development and licensing teams

- Competitive intelligence teams

- Market access and HEOR teams

- Equity research and biotech investors

- Oncology pipeline and portfolio teams

- Consulting firms working in lung cancer, immuno-oncology, or bispecific antibodies

Additional information

| Price | Single User License, 2-3 User License, Site License, Enterprise License |

|---|

Table of Contents

Chapter 1. Ivonescimab (AK112/SMT112) in Non-Small Cell Lung Cancer……………………… 5

- The Clinical Foundation: What Changed at ASCO 2026…………………………………………………………. 5

- The HARMONi-3 Inflection Point: Five Updated Scenarios……………………………………………………. 9

- The Mechanistic Moat: Why the 18x Amplification Matters…………………………………………………… 10

- The Competitive Landscape: The Race Has Accelerated……………………………………………………….. 11

- Real-World Evidence: The 70,000-Patient Advantage…………………………………………………………. 12

- Commercial Strategy: From Niche to Blockbuster………………………………………………………………. 12

- KOL and Analyst Sentiment: The Consensus and the Controversies…………………………………………. 14

- Catalyst Calendar: What to Watch in H2 2026 and Beyond…………………………………………………… 14

- Investment and Strategic Recommendations…………………………………………………………………….. 15

- Conclusion: A Watershed Moment with Uncertain Tides…………………………………………………….. 16

Chapter 2. Disease Background…………………………………………………………………………………… 17

2.1 Epidemiology: Global Burden, US Incidence, and Why This Market Matters…………………………….. 17

2.2 Molecular Subtypes: Why NSCLC Is Actually Many Different Diseases……………………………………. 18

2.3 PD-L1 Testing: The Gatekeeper to Modern Treatment……………………………………………………….. 19

2.4 The 2L Post-TKI EGFR Setting: Ivonescimab’s Regulatory Beachhead……………………………………. 20

2.5 The Squamous NSCLC Battleground: Where HARMONi-6 Changed History……………………………. 22

2.6 The Perioperative Revolution: Treating Lung Cancer Before It Spreads…………………………………… 23

2.7 The Competitive Treatment Algorithm: Where Ivonescimab Fits…………………………………………… 24

2.8 Conclusion: The Disease Context for Ivonescimab’s Commercial Opportunity…………………………… 26

Chapter 3. Mechanism of Action………………………………………………………………………………….. 28

3.1 Drug Architecture: The Tetravalent Fc-Silent Bispecific Design…………………………………………….. 28

3.2 The VEGF Immunosuppression Pathway (Mechanism 1)……………………………………………………. 30

3.3 The PD-1 Checkpoint Pathway (Mechanism 2)…………………………………………………………………. 31

3.4 The Cooperative Binding Amplification Effect: The 18x Differentiator…………………………………….. 32

3.5 The Pennell-Bteich Critique: Is This Just a VEGF Effect?……………………………………………………. 34

3.6 Conclusion: Mechanism as Commercial Moat………………………………………………………………….. 36

Chapter 4. The Full HARMONi Clinical Programme………………………………………………………. 38

4.1 Programme Architecture: Why Seven Trials Matter…………………………………………………………… 38

4.2 HARMONi: The BLA Foundation — Summit’s Near-Term Revenue Floor……………………………….. 39

4.3 HARMONi-A: First Phase 3 OS Confirmation — The Chinese Validation…………………………………. 40

4.4 HARMONi-2: Ivonescimab vs. Keytruda Monotherapy — The Head-to-Head Proof……………………. 41

4.5 HARMONi-6: The ASCO 2026 Plenary — The Trial That Made History…………………………………… 42

4.6 HARMONi-3: The Western First-Line Binary — The Trial That Determines Everything………………. 44

4.7 HARMONi-7 and Emerging Trials: The Insurance Policy and the Future…………………………………. 45

4.8 The Fifteen Phase 3 Studies: Akeso’s Global Ambition……………………………………………………….. 46

4.9 Conclusion: The Portfolio as Value Driver………………………………………………………………………. 47

Chapter 5. Company Profiles……………………………………………………………………………………….. 48

5.1 Akeso, Inc. (HKEX: 9926.HK) — Innovator and China Commercialiser…………………………………… 48

5.2 Summit Therapeutics (NASDAQ: SMMT) — Global Development and Commercial Partner………….. 50

5.3 The Akeso-Summit Licensing Deal — Structure, Economics, and Strategic Implications………………. 52

5.4 Strategic Implications: Why This Partnership Matters……………………………………………………….. 54

5.5 Conclusion: The Partnership as Competitive Advantage……………………………………………………… 56

Chapter 6. HARMONi-3 Prediction Framework…………………………………………………………….. 57

6.1 Why the HARMONi-3 Interim Miss Is Not Biologically Definitive………………………………………….. 57

6.2 Biological Conditions for Western Mechanism Translation………………………………………………….. 58

6.3 Scenario A (35%): Positive — PFS HR 0.70 to 0.76, OS Trending Favourable……………………………. 59

6.4 Scenario B (28%): Strong Positive — PFS HR 0.62 to 0.68, Early OS Signal Emerges………………….. 60

6.5 Scenario C (22%): Marginal Positive — PFS HR 0.78 to 0.85, OS Inconclusive………………………….. 61

6.6 Scenario D (10%): Negative — PFS HR >0.85 or Directionally Negative………………………………….. 62

6.7 Scenario E (5%): Data Delayed to Q1 2027……………………………………………………………………… 63

6.8 Probability-Weighted Expected Peak U.S. Revenue — $978M Central Estimate………………………… 63

6.9 Updated Scenario Probabilities Post-ASCO 2026……………………………………………………………… 64

6.10 Conclusion: The Scenario Framework as Investment Tool…………………………………………………. 65

Chapter 7. KOL Sentiment Analysis…………………………………………………………………………….. 67

7.1 Methodology: How We Map the KOL Landscape………………………………………………………………. 67

7.2 The Four Prescribing Camps and Their Commercial Implications………………………………………….. 68

7.3 The Brahmer Discussant Analysis — What She Said and What It Means Commercially………………… 71

7.4 The Pennell-Bteich Sceptic Argument — Stakes, Evidence, and Counterargument……………………… 72

7.5 The Singhi Sequencing Question — The Most Commercially Precise KOL Comment……………………. 73

7.6 KOL Sentiment as a Leading Indicator of Commercial Adoption…………………………………………… 74

7.7 Conclusion: KOL Sentiment as a Dynamic Variable…………………………………………………………… 75

Chapter 8. Regulatory Landscape……………………………………………………………………………….. 77

8.1 US FDA — BLA Under Review, PDUFA November 14, 2026…………………………………………………. 77

8.2 IRA Pricing Risk — Favourable Biologic Timing……………………………………………………………….. 79

8.3 FDA Mid-Cycle Communication — What to Watch (August 2026)…………………………………………. 80

8.4 European EMA Pathway……………………………………………………………………………………………. 80

8.5 Japan PMDA Pathway………………………………………………………………………………………………. 81

8.6 China NMPA — Already Approved and Commercially Active……………………………………………….. 82

8.7 Conclusion: Regulatory Strategy as Competitive Moat……………………………………………………….. 84

Chapter 9. Market Sizing and Revenue Model………………………………………………………………. 85

9.1 Global NSCLC Market Context: The Scale of the Prize………………………………………………………… 85

9.2 Seven-Layer US Patient Funnel: From Incidence to Addressable Market…………………………………. 86

9.3 US Revenue Model: Five Scenario P&L………………………………………………………………………….. 87

9.4 Net Price Assumptions and the IRA Framework………………………………………………………………. 89

9.5 Royalty Structure: The Akeso Share……………………………………………………………………………… 91

9.6 Revenue Ramp and Time-to-Peak………………………………………………………………………………… 91

9.7 International Revenue: Beyond the US………………………………………………………………………….. 92

9.8 Conclusion: The Revenue Model as Investment Compass……………………………………………………. 93

Chapter 10. Payer Access and HTA Analysis……………………………………………………………….. 95

10.1 The Global Payer Landscape: Why Access Matters as Much as Efficacy………………………………….. 95

10.2 US CMS/PBM: The Market That Matters Most……………………………………………………………….. 96

10.3 UK NICE: The Cancer Drugs Fund Pathway…………………………………………………………………… 98

10.4 Germany G-BA: The AMNOG Gauntlet………………………………………………………………………… 99

10.5 France HAS: The ASMR Rating System………………………………………………………………………. 100

10.6 Italy AIFA: The Innovation Status Pathway………………………………………………………………….. 101

10.7 Spain AEMPS: The GENESIS and Regional Challenge…………………………………………………….. 102

10.8 Japan NHI: The Asian Proximity Advantage………………………………………………………………… 102

10.9 China NRDL: Already Active, Already Pricing-Constrained………………………………………………. 103

10.10 Conclusion: Payer Access as Competitive Moat……………………………………………………………. 104

Chapter 11. The Sacituzumab Tirumotecan Threat……………………………………………………… 106

11.1 OptiTROP-Lung05: Full Data Analysis………………………………………………………………………… 106

11.2 The Head-to-Head Comparison: Ivonescimab vs. Sac-TMT……………………………………………….. 108

11.3 Patient Population Overlap and Competitive Partition…………………………………………………….. 109

11.4 The Merck Factor: Why Sac-TMT Is More Dangerous Than It Appears…………………………………. 110

11.5 The 2028 Three-Way Market Partition Model……………………………………………………………….. 111

11.6 Merck MK-2010: The Third PD-1/VEGF Bispecific…………………………………………………………. 112

11.7 The Strategic Implications for Summit………………………………………………………………………… 112

11.8 Conclusion: The Competitive Landscape Is Now Three-Dimensional……………………………………. 113

Chapter 12. Competitive Landscape…………………………………………………………………………… 115

12.1 Current Standard of Care by Patient Segment: 2026 Baseline…………………………………………….. 115

12.2 Keytruda: The $8B Franchise and Where It Is Threatened……………………………………………….. 116

12.3 The Emerging Competitors: Beyond Keytruda and Ivonescimab………………………………………… 118

12.4 to 12.7 The Treatment Algorithm Across Four Time Horizons……………………………………………. 120

12.8 Conclusion: The Competitive Landscape as Strategic Map………………………………………………… 125

Chapter 13. Deal Intelligence and Business Development Opportunity………………………. 126

13.1 Comparable Transaction Benchmarks…………………………………………………………………………. 126

13.2 The Akeso-Summit Partnership Structure and Its Implications………………………………………….. 127

13.3 Acquirer Fit Ranking: Top Five Strategic Buyers……………………………………………………………. 128

13.4 The Pre-Data BD Window and Certainty Premium…………………………………………………………. 131

13.5 Deal Structure Considerations………………………………………………………………………………….. 133

13.6 Conclusion: The Transaction Imperative……………………………………………………………………… 133

Chapter 14. Sensitivity, Scenario Analysis…………………………………………………………………. 135

14.1 US Peak Revenue Sensitivity Matrix…………………………………………………………………………… 135

14.2 China Royalty Sensitivity and Akeso Economics…………………………………………………………….. 136

14.3 The Decision Dashboard: What to Watch, When, and What It Means………………………………….. 137

14.4 Scenario Probability Distribution and Expected Value…………………………………………………….. 138

14.5 Sac-TMT Competitive Threat Analysis: The Emerging Three-Player Market………………………….. 138

14.6 Cross-Scenario Risk Factors…………………………………………………………………………………….. 139

14.7 The Investment Committee Briefing…………………………………………………………………………… 140

14.8 Conclusion: The Asymmetric Risk/Reward Profile…………………………………………………………. 142

Chapter 15. Strategic Implications……………………………………………………………………………… 144

15.1 For Pharma Commercial and Medical Affairs Teams……………………………………………………….. 144

15.2 For Business Development and Licensing Teams…………………………………………………………… 145

15.3 For Equity Research and Portfolio Managers………………………………………………………………… 147

15.4 For Market Access and HTA Teams……………………………………………………………………………. 147

15.5 For Biotech R&D and Pipeline Teams…………………………………………………………………………. 149

15.6 For Competitive Intelligence and Strategy Teams…………………………………………………………… 150

15.7 For Investors in the Biotech Ecosystem……………………………………………………………………….. 150

15.8 Conclusion: The Action Imperative……………………………………………………………………………. 151

Related products

-

Complex regional pain syndrome (CRPS)| Primary Research (KOL’s Insight) | Market Intelligence | Epidemiology & Market Forecast-2032

Price range: $6,989.00 through $20,967.00Select options This product has multiple variants. The options may be chosen on the product pageComplex regional pain syndrome (CRPS) is a chronic pain condition characterized by spontaneous and evoked regional pain, usually starting in a distal extremity, which is disproportionate in magnitude or duration to the typical pain course after similar tissue trauma. Current treatment for CRPS requires a multidisciplinary approach involving patient education, physical and occupational therapy, psychiatry and pain medicine specialists, along with pharmacological and surgical interventions. Unfortunately, the current available treatment options are generally considered to be ineffective and one-dimensional, as they only treat part of the disease. Emerging therapies like Soticlestat (Takeda / Ovid Therapeutics and Lanicemine (AstraZeneca / Biohaven Pharmaceuticals) is expected to generate more market share than other emerging therapies and have the potential to overcome the treatment barrier.

-

Obstructive Sleep Apnea (OSA) | Primary Research (KOL’s Insight) | Competitive Intelligence | Market Analytics & Forecast 2032

Price range: $6,989.00 through $20,967.00Select options This product has multiple variants. The options may be chosen on the product pageGrowth of the Prevalence OSA population will contribute to increasing sales in the OSA therapy market over our forecast period. The increase in the number of patients with obstructive sleep apnea across the globe will be driving the market of OSA. According to a study conducted by the World Health Organization (WHO), the global prevalence of sleep apnea is around 100 million people. In the U.S. alone, the number of people with OSA is around 42 million. One out of five adults in the U.S. has mild OSA, while one out of 15 has moderate to severe OSA. The number of cases with OSA is expected to increase during our forecast period, primarily due to the increasing Prevalence of sleep-related disorders. This is projected to drive the OSA market from 2022 to 2032

-

Prader-Willi Syndrome (PWS)| Primary Research (KOL’s Insight) | Market Intelligence | Epidemiology & Market Forecast-2032

Price range: $6,989.00 through $20,967.00Select options This product has multiple variants. The options may be chosen on the product pageThe Prader-Willi Syndrome (PWS) market is hugely contributed by current standard of care (human growth hormone therapy) as there is no cure for PWS. By 2032, the market is expected to change due to the uptake and launch of new novel therapies. In a PWS treatment setting, the current SoC will decline, and the novel emerging drugs will grasp the highest market shares. The sales of the emerging therapies for the treatment of PWS in the study countries (United States, France, Germany, Italy, Spain, United Kingdom and Japan) will experience high growth over the 2018-2032 study period, adding a value estimated at a total market of $ 2.1 billion by 2032.

-

ER+/HER2- Metastatic Breast Cancer (mBC)| Primary Research (KOL’s Insight) | Market Intelligence | Epidemiology & Market Forecast-2032

Price range: $6,989.00 through $20,967.00Select options This product has multiple variants. The options may be chosen on the product pageThe ER + / HER2- metastatic breast cancer (mBC) market is relatively large with the highest market share holding CDK4 / 6 drugs, e.g. Pfizer’s Ibrance (palbociclib), Novartis’s Kisqali (ribociclib) and Eli Lilly’s Verzenio (abemaciclib). By 2032, these drugs will continue to hold the largest share of the market, but we also expect the market to expand with the addition of new oral SERDs/SARMs/SERMs that will take a combined share of 19.1%, antibody drug conjugates with a share of the 2.9% and AKT inhibitors with a 2.6% share. The sales of the emerging therapies for the treatment of ER+/HER2- mBC in the study countries (United States, France, Germany, Italy, Spain, United Kingdom and Japan) will experience high growth over the 2022-2032 study period, adding a value estimated at a total market of $ 5.6 billion by 2032.