English

English Semaglutide: Real-World KOLs Opinions Seem Divided!

Rising global OBESITY concerns spotlight Novo Nordisk’s Semaglutide, a key topic among many analysts. Semaglutide brings forth the best possibilities when it comes to weight loss. On average, patients experienced a weight loss of approximately 17.7% by week 60 when using the injection formulation. Impressive, isn’t it?

Novo Nordisk is expected to submit regulatory filings for the 25 mg and 50 mg oral semaglutide versions by the end of 2023 or early 2024. If approved, the oral form could enhance patient compliance and ensure a stable presence in the market.

Considering these developments, Semaglutide has a substantial opportunity to become a blockbuster drug, because more than 50% of the world’s population will be living with either overweight or obesity by 2035 as per World Obesity Federation. About 1 in 4 people (nearly 2 billion) will have obesity.

The economic implications are profound. According to the World Obesity Atlas 2023 report, the global economic impact of overweight and obesity will reach $4.32 trillion annually by 2035 if prevention and treatment measures do not improve.

WOA report

Now that we have laid the foundation for Semaglutide, let’s deep dive into how the competition is evolving in the Obesity Space.

Mellalta’s Take: Obesity Competitors Vs Semaglutide

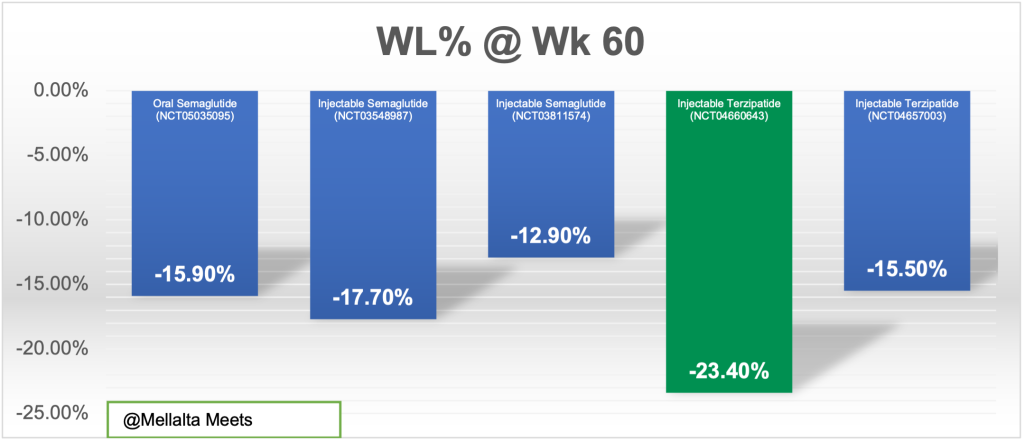

Currently, none of the products are compared head-to-head and therefore, the current study designs are influencing the outcomes. Also, not all the drugs have the reported outcomes till week 60; so we have compared only two drugs for which the data is available. The results speak for themselves: Lilly’s tirzepatide has edged out Novo’s Semaglutide.

The graph shows the Weight Loss Among Obese Persons and Obese (Type 2 Diabetes)T2D patients by Therapeutic Approach (60 Weeks) comparing two drugs Semaglutide and Terzipatide.

Obesity Milestones/Catalysts to Watch for!

The obesity landscape is becoming increasingly crowded with continually rising expectations. We anticipate that emerging companies focusing on these potential differentiations, particularly with combinable incretins (e.g., GLP-1, GIP, GCG, PPY) and complementary non-incretin MOAs, could capture a meaningful market share in the future.

| Drug | Company | Headquarters | MOA | Catalyst/Milestones | Catalyst/Milestones Timeline |

|---|---|---|---|---|---|

| Mounjaro (Tirzepatide) | Eli Lilly | Indiana, United States | GLP-I/GIP | Additional Ph3 SURMOUNT-4 Data (at EASD) | Oct ’23 |

| Mounjaro (Tirzepatide) | Eli Lilly | Indiana, United States | GLP-I/GIP | Additional Ph3 SURMOUNT-3 data (at Obesity Week) | Oct ’23 |

| Wegovy (Semaglutide) | Novo Nordisk | Denmark | GLP-I | Detailed SELECT cardiovascular outcomes data (at AHA) | Nov ’23 |

| Oral semaglutide (Rybelsus) | Novo Nordisk | Denmark | GLP-I | Potential regulatory filings Of 25 mg and 50 mg oral semaglutide | 2023/2024 |

| Pemvidutide | Altimmune | Maryland, United States | GLP.I/GCG | Top line 48-week data for Ph2 MOMENTUM trial | 4Q23 |

| Oral VK2735 | Viking Therapeutics | California, United States | GLP-I/GIP | Phl data in healthy volunteers | 4Q23 |

| Danuglipron | Pfizer | New York, United States | GLP-I | Ph2b completion | 4Q23 |

| GSBR-1290 | Structure Therapeutics | California, United States | GLP-I | Top line 12-week Ph2a and Phlb MAD data Obesity/T2D | 4Q23 |

| Survodutide | Boehringer Ingelheim and Zealand Pharma | Germany & Denmark | GLP-I/GCG | Potential Ph3 initiation | 2023/2024 |

| Mounjaro (Tirzepatide) | Eli Lilly | Indiana, United States | GLP.I/GIP | Potential completion of NDA rolling submission and approval in obesity | 2023/2024 |

| AMG133 | Amgen | California, United States | GLP-1/GlP-antagonist | Potential Ph2 data | 2023/2024 |

And what are the most critical factors that have a huge market as well as Payer implications in Obesity space?

Weight Rebound:

- Semaglutide drug has proven its efficacy and potential by showcasing about 14% to 20% reduction in weight. But the weight loss is generally not sustained upon discontinuation and will rebound by 2X or 3X.

- This case is not just with Semaglutide, but all the potential GLP-1 which are in the pipeline.

- Now if the company has to sustain the efficacy, then the patient should be put on the drug for a long time– could be for a lifetime.

For such a prolonged treatment approach to be viable, GLP-1 tolerability is critical.

GLP-1 Tolerability:

- KOLs emphasized the need for the weight loss to be maintained for long-term benefit, stating that 75-80% of the benefit will be gone should the patient not be able to maintain the weight improvement. Thus, the issue of GLP-1 tolerability is critical to sustaining the weight reduction.

- Also, they predict that 50% of patients would not be able to sustainably take GLP-1 medications and cited the difficulty of tolerating side effects and the administration burden of a weekly injection.

Now Oral-based therapies could be an answer to reduce the burden!

Oral vs Injections:

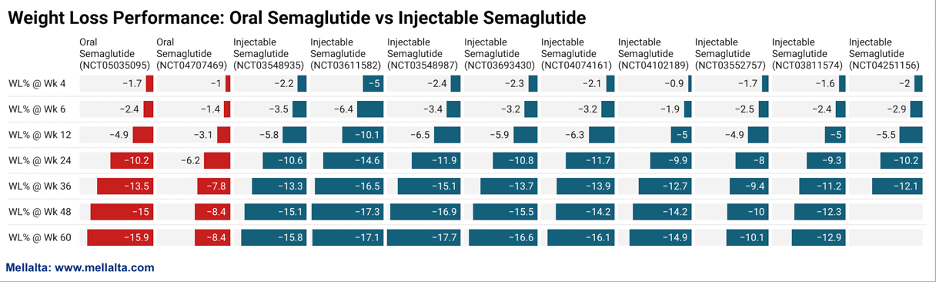

Currently, Semaglutide oral formulation is showing an impressive 15.9% reduction in weight at week 60 slightly lower than the injectables which is 17.9% at week 60.

Let’s build scenarios!

Scenario 1: In case if there is an improved version or Oral formulation with similar or higher efficacy compared to the injectables are approved?

- This would represent a significant breakthrough.

- We see penetration would be much greater under this scenario, given that the orals would likely have less of the side effects (nausea, vomiting, diarrhea, constipation, lack of desire to eat any food) or even a monthly injectable (to decrease injection fear burden).

- Not only this, but Oral also/ small molecule options could provide better convenience/ compliance, and increased supply due to easier manufacturing, leading to potentially lower prices and greater access.

Another scenario, what if the Oral formulation doesn’t make it to the market, then what options we have?

- Combinable incretins (e.g., GLP-1, GIP, GCG, PPY) that could generate higher efficacy while balancing safety/tolerability;

- Complementary non-incretin MOAs (e.g., ActRII, mitochondria) that could further enhance the drug profile such as preserving lean muscle, and prolonging durability.

The last but the most critical factor is coverage.

Coverage under Medicare Part D for Obesity Drugs

There is a long debate ongoing for the coverage of obesity drugs under Medicare Part D. The opponents are more worried that covering GLP-1 agonists for obesity would have an unsustainable budget impact. However, a recent paper authored by William Shrank, Serena Jingchuan Guo, and Davene R. Wright, PhD, critically assesses these concerns.

Important arguments complied from the paper by Inmaculada (Inma) Hernandez, are as follows:

- Critics believe that covering GLP-1 agonists for obesity would strain the budget. Yet, these concerns overlook:

- cost offsets associated with prevented complications

- decrease in net prices as more agents enter the market

- Medicare price negotiation (if Ozempic is negotiated, as expected, Wegovy would automatically be subject to negotiation if it was covered under Part D)

- future entry of generics

- Public funding should not be used to support treatment given personal responsibility. However, public payers pay for smoking cessation, and other drugs for metabolic syndrome manifestations are considered of such high value that Part D plans are rewarded for beneficiary adherence (in fact, GLP1s approved for Type 2 Diabetes are included in a star rating measure)

- Discuss policy options for Part D coverage:

- Legislative change. The most relevant bill in this regard is the Treat and Reduce Obesity Act, recently reintroduced in Congress.

In a scenario where GLP-1s are potentially covered by Medicare Part D, KOLs believe that this will make a bigger impact once obesity is treated more like a disease and treatment becomes part of guidelines, allowing prescribers to reliably consider them as options.

Currently, some patients are paying up to $1,000 out-of-pocket for GLP-1s, which means the coverage debate is a significant concern that’s anticipated to continue over the next 1-2 years.

Mellalta’s Conclusion

Though Obesity is an exciting space, it also comes with its repercussions. Companies have to put efforts into convincing KOLs, HCPs as well and payers to continuously support patient uptake. Several critical factors including real-world adherence, cost barriers, uncertainty surrounding widespread payer coverage, higher study dosages compared to real-world use, and gastrointestinal side effects affecting treatment tolerance, still remain questionable.